Gift Aid is a tax relief scheme which allows UK charities to reclaim an extra 25% in tax on every eligible donation made by a UK taxpayer.

If you are a UK taxpayer, your contribution to a donor-advised fund (DAF) may benefit from Gift Aid. Both NPT UK and NPT Transatlantic, as UK registered charities, can claim 25 pence through Gift Aid for every £1 contributed.

As a result, the value of your donation is automatically increased by 25%, meaning you can give more to the causes you care about.

Gift Aid also allows higher tax rate payers to claim tax relief for themselves through their tax return, in respect of the tax they have paid over and above basic rate tax.

How Does Gift Aid Work?

Under the Gift Aid scheme, the donor and beneficiary charity can reclaim taxes the donor paid to HM Revenue & Customs (HMRC).

For example, here is how claims would work for donations of £100, £1,000, and £10,000:

| Donation Amount | Charity Claims | Total Received by Charity | Taxpayer's Tax Relief |

|---|---|---|---|

| £100 | £25 | £125 | Basic rate (20%): None Higher rate (40%): £25 (£125 x 20%) Additional rate (45%): £31.25 (£125 x 25%) |

| £1,000 | £250 | £1,250 | Basic rate (20%): None Higher rate (40%): £250 (£1,250 x 20%) Additional rate (45%): £312.50 (£1,250 x 25%) |

| £10,000 | £2,500 | £12,500 | Basic rate (20%): None Higher rate (40%): £2,500 (£12,500 x 20%) Additional rate (45%): £3,125 (£12,500 x 25%) |

As registered UK charities, both NPT UK and NPT Transatlantic are eligible to claim an amount equal to basic rate tax (20%) on the gross gift from HMRC, which equates to 25% of the value of the donation.

NPT UK and NPT Transatlantic will claim Gift Aid on your contribution and credit your donor-advised fund account for the amount of the reclaimed Gift Aid.

Donors who are higher-rate (40%) or additional rate (45%) taxpayers are eligible to claim the difference between their tax rate and the basic tax rate (20%) on the gross donation and can claim this on their self-assessment tax return.

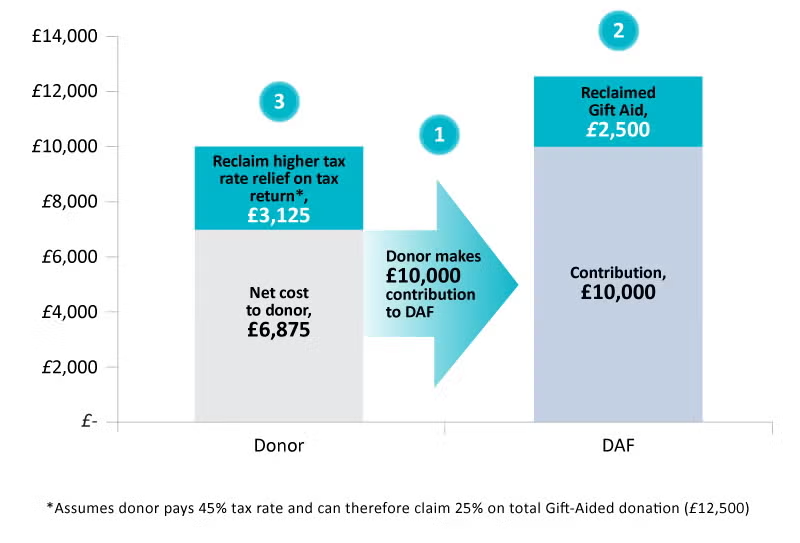

For a donor who is an additional rate taxpayer, a donation of £10,000 provides the DAF with £12,500 for a net cost of £6,875.

How Do You Qualify?

To qualify for Gift Aid, the donor must:

- Be a UK taxpayer

- Make cash contributions

- Pay enough UK income and/or capital gains tax in each tax year to cover the amount of tax that charities claim on your behalf for that tax year

- Complete a Gift Aid declaration form

- Only claim Gift Aid on new donations to charity. Transfers to a DAF from another DAF programme, a charitable foundation, or another charitable giving vehicle are not eligible for Gift Aid.

Gift Aid and Donor-Advised Funds

Leveraging a DAF allows donors to maximise the benefits of Gift Aid on eligible cash contributions, enhancing the impact of charitable giving while simplifying administration and tax relief claims.

By choosing either an NPT UK or NPT Transatlantic DAF, you can streamline your philanthropy and make the most of your UK tax incentives.

You can open a DAF account online in minutes, or contact us to learn more.

FAQs About Gift Aid

To qualify for Gift Aid, the donor must make a cash donation, which can also be via a direct debit, standing order or bank transfer.

No. Any donation made with a company or other people’s money through fundraising events are not eligible for Gift Aid.

Yes. You can support as many UK charities as you like through Gift Aid. You just need to ensure you are paying enough tax during the year to cover your total annual donations and submit a return declaration for each charity you support.

Donations made to charity through payroll giving are not eligible for Gift Aid. Payroll giving donations are taken from your wages before tax.

Please Note: The information provided here is general and educational in nature. It is not intended to be, nor should it be construed as, legal or tax advice. NPT UK does not provide legal or tax advice. NPT UK strongly encourages you to consult with your tax and/or legal advisors before making charitable contributions.

Last Updated: May 2026